Market & Economic Commentary: Q4 2023

Quarter in Review

In 2023, the year concluded with a remarkable turnaround, characterized by a year-end surge driven by the collective relief that the U.S. economy had managed to steer clear of the recession many had feared would dominate the year. Contrary to expectations of consumers retrenching and stalling economic growth, they defied economists’ predictions by continuing their spending habits. This resilience, coupled with the easing of inflationary pressures, acted as a catalyst for the economy’s positive momentum. As the year drew to a close, the reduction in inflation, brought about by higher interest rates, led to a moderation in interest-rate expectations for 2024 and may possibly even enable rate cuts.

The broad US markets shook off one of the worst October performances in years to finish strongly in the last few months of 2023. With gains in all three major US market indexes, as well as in fixed income, investors were able to recoup some of the portfolio losses experienced in 2022.

The year-end culminated with the S&P 500 up 24%. The Dow Jones Industrial Average climbed 14% and the NASDAQ Composite, fueled by the excitement surrounding artificial intelligence, gained 43% for the year. 1

Bond markets also participated in the rally, and as a result of the rise in bond prices, yields on 10-year U.S. Treasuries, a widely recognized global borrowing benchmark, significantly declined by over 110 basis points since their peak of 5.02% in October to finish the year at 3.87%. 2

The Large Impact of the Few

While the headline performance of the S&P 500 and the Nasdaq were certainly outstanding, the bulk of the performance was driven by just a small handful of stocks. The “Magnificent Seven” (Apple, Microsoft, Google parent Alphabet, Amazon.com, Nvidia, Meta Platforms and Tesla) contributed 60% of the index’s performance. 3 Eli Lily can be added to this group as it was up 57.4%. These eight stocks primarily benefited from the exuberance around Artificial Intelligence and declining interest rates that make their future growth more valuable. Eli Lily, of course, rose the Semaglutide wave.

Notably, an index comprised of the same S&P 500 stocks but given equal weights rather than weights dictated by market capitalization, returned 13.9% for full year 2023. Fully, 72% of the stocks that make up the index underperformed the index in 2023. 4 The wide dispersion in results can be seen in the varied performance of the sectors that comprise the broad market. As shown below, while technology stocks returned 56% for the year (contributing to the Nasdaq’s 43% return), utilities, consumer staples, and energy stocks actually lost money.

1 Banerji, G., “What Did Wall Street Get Right About Markets This Year? Not Much,” Wall Street Journal, December 29, 2023. https://www.wsj.com/finance/stocks/ what-did-wall-street-get-right-about-markets-thisyear-not-much-7d4368fe

2 Carson, R. & Kondo, M., “Global Bond ‘Carnival’ Sets Stage For Record Two Months,” Bloomberg.com, December 28, 2023. https://www.bloomberg.com/news/ articles/2023-12-28/global-bonds-eye-biggest-evertwo-month-gain-amid-rate-cut-bets

3 https://on.spdji.com/rs/838-LDP-483/images/dashboard-sp-500-factor-2023-12.pdf?mkt_tok=ODM4LUxEUC00ODMAAAGQabL6K-BCGP1X0i2kkijiZpogvc1oYbAB6-Hn9iR4SWYmszeT8EkcJCNazRm7mBAtBi84bQmyg-JzF0uKQOlQf2iq49mOtu1idys-mJTsCCQ

4 https://finance.yahoo.com/news/kind-incredible-power-almost-75-120000098.html

The same divergence in performance was evident in the results of global stock markets.

The result has been that, despite the headline double digit growth of the S&P 500 and the tech-heavy Nasdaq, a globally diversified stock portfolio would have returned less than the market average in 2023.

Nevertheless, the long-term argument for diversification remains compelling. The same handful of stocks that led the market up in 2023 also declined by more than the market average in 2022, down 46% compared with the 19% decline in the S&P 500. 6 Meanwhile concentrating investments in a small universe of companies entails considerable company-specific and sector-specific risk over time. In this case, having reacted with excitement to the wide-spread embrace of AI, this group of companies will have to prove that they can monetize this interest, with few clear and obvious paths yet to emerge. Further, the risk of future restrictions on deals with the large Chinese industrial and consumer markets adds uncertainty. With valuations stretched to expensive levels in the highest-flying stocks of 2023, we would counsel investors to maintain exposure to the less-expensive parts of the market for consistent growth over time.

5 https://on.spdji.com/rs/838-LDP-483/images/dashboard-us-sector-2023-12.pdf?mkt_tok=ODM4LUxEUC00ODMAAAGQatNWOUi0ptiusZVmFtcs6bPluPDAAKYM_X23_qXvv2izvuRikcCD9idg94ILbFxjFJ1J2yPHo_CefiL-67VJzNr4HV6j8rSp3fecgur1uI

6 https://www.investmenttalk.co/p/is-it-really-just-the-mag-7

Economic Growth Persists but Pessimism Endures

The U.S. economy showed steady growth in 2023. It expanded at an average annualized rate of 3.2% in the first three quarters, and another 1.3% is projected for Q4. In November, headline inflation decreased to 3.1%, although it inched back up to 3.4% in December. With housing costs a lagging factor in the index, future rates of inflation are expected to be lower.

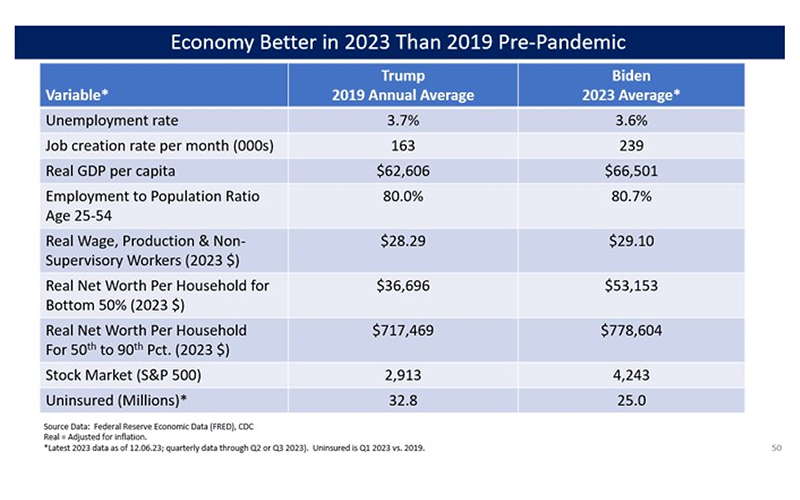

Meanwhile the job market has remained robust, exceeding expectations. Together, increasing incomes and decelerating inflationary pressures should help consumers retain some spending power into 2024. Indeed, the data for 2023 compared with 2019 show a favorable economic dynamic that should set the stage for a strong 2024.

Despite the growing economy, a tension has emerged between the data and public views of the economy: poll respondents consistently express pessimism about the current or future economic situation, to the extent that a new word “Vibecession” has been added to the lexicon. To a small degree, higher debt levels and resumed student loan repayments could be supplying some headwinds. Still, the concept of Vibecession epitomizes what seems to be a pervasive disconnect between people’s perceptions and objective economic indicators. While it seems to have had little to no effect on consumer spending or markets thus far, it bears watching as a potential source of shifting investor sentiment and volatility during a contentious political season in 2024.

Final Thoughts

The past four years have been a rollercoaster ride for markets as the world has reacted to a pandemic, inflationary aftershocks, wars in Europe and the Middle East, and historic central bank activity.

However, we remind clients that multi-year periods in the markets have usually been driven by seemingly momentous events: financial crises, natural disasters, political turmoil, and geopolitical realignments. Markets have reflected this with inevitable volatility. Still economies have adapted, and technological advances, demographic growth, and consumer engagement have ultimately driven economic growth - and markets - higher.

As with riding a rollercoaster, trying to time the ups and downs of the ride, and getting off while it’s in motion is how you get hurt. The best action is to stay on the ride until you reach the final destination.

Enjoy the highs, endure the lows, and focus on your long-term goals.

Index Disclosure and Definitions

Investors cannot invest directly in an index. Indexes have no fees. Historical performance results for investment indexes do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the occurrence of which would have the effect of decreasing historical performance results. Actual performance for client accounts will differ from index performance.

S&P 500 Index represents the 500 leading U.S. companies, approximately 80% of the total U.S. market capitalization.

Dow Jones Industrial Average (DJIA) Is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange (NYSE) and the NASDAQ.

The Nasdaq Composite Index (NASDAQ) measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market and includes over 2,500 companies.

MSCI World Ex USA GR USD Index captures large and mid-cap representation across 22 of 23 developed markets countries, excluding the US. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets (as defined by MSCI). The index consists of the 25 emerging market country indexes. Bloomberg Barclays US

Aggregate Bond Index measures the performance of the U.S. investment grade bond market. The index invests in a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States – including government, corporate, and international dollardenominated bonds, as well as mortgage-backed and asset-backed securities, all with maturities of more than 1 year.

Bloomberg Barclays Global Aggregate (USD Hedged) Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging market issuers. Index is USD hedged.

© Morningstar 2021. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied, adapted or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information, except where such damages or losses cannot be limited or excluded by law in your jurisdiction. Past financial performance is no guarantee of future results.

The Kaminsky-Silverman Group utilizes Symmetry Partners, LLC (SP), which is a third-party service provider that supplies market data and assists in creation and monitoring of factor-based investment models. SP is also an investment advisory firm registered with the Securities and Exchange Commission (“SEC”). All data is from sources believed to be reliable but cannot be guaranteed or warranted. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product or any non-investment related content referenced, directly or indirectly, in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may not be reflective of current opinions or positions. Please note the material is provided for educational and background use only. Moreover, you should not assume that any discussion or information contained in this material serves as the receipt of, or as a substitute for, personalized investment advice.

Diversification seeks to improve performance by spreading your investment dollars into various asset classes to add balance to your portfolio. Using this methodology, however, does not guarantee a profit or protection from loss in a declining market. Past performance does not guarantee future results.

This material is confidential and is provided for informational purposes only and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Investment return and principal value of an investment will fluctuate; therefore, you may have a gain or loss when you sell your investment. Any opinions, expectations and projections within this document are solely those of the Portfolio Manager(s) identified, and do not necessarily represent the viewpoint of Shufro, Rose & Co., LLC or other Portfolio Managers at the firm. This report was prepared by Shufro, Rose & Co., LLC and is presumed to be correct. Shufro, Rose & Co., LLC is an investment adviser registered with the SEC. ADV Part 2A is available upon request or at https://adviserinfo.sec.gov/. Please contact Shufro, Rose & Co., LLC at (212) 754-5100 with any questions.